|

ThinkingApplied.com

|

|

Mind Tools: Applications and Solutions |

When

More Is Less:

A Taxing Tale of Trading (in Three Acts)

Download

as PDF file

Prologue

A family drama is about to unfold. Simultaneously, a husband and a wife make separate, but identical, investments. In the months that follow, they implement very different strategies.

Act 1, Scene 1

The

Husband's Tale

(See Fig. 1)

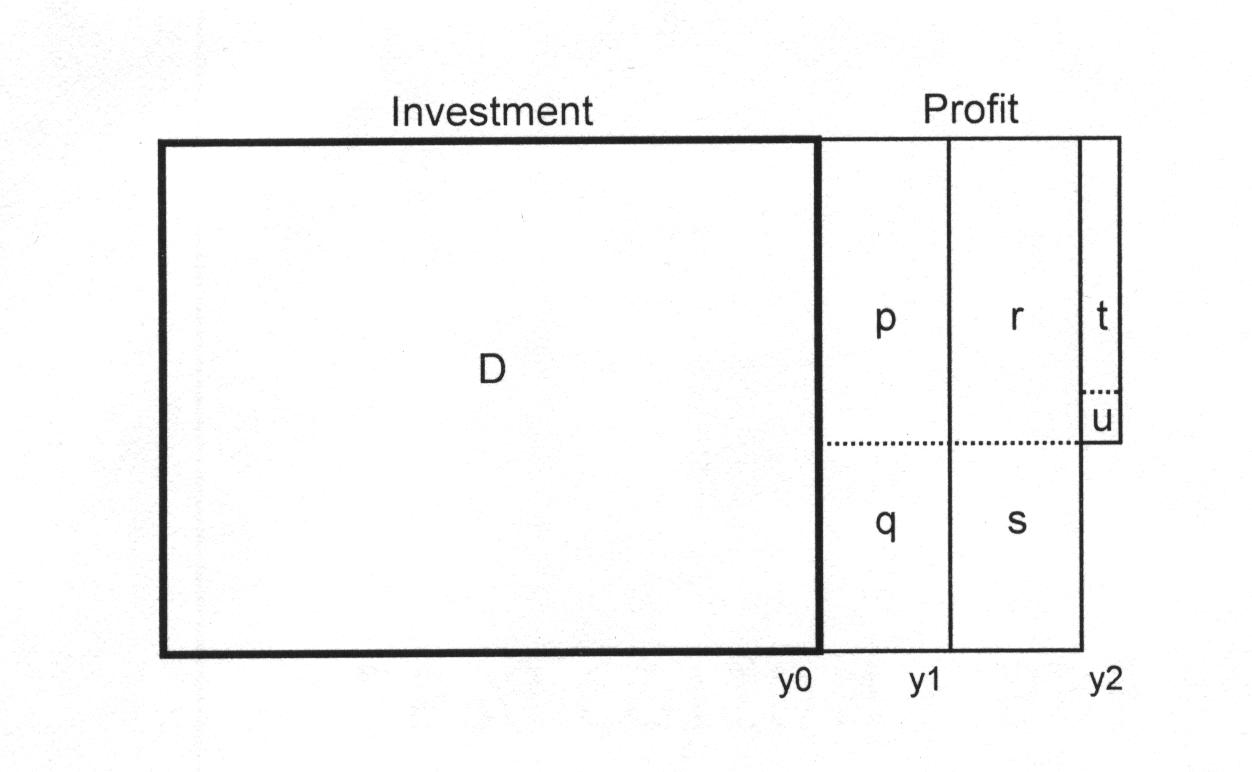

Fig. 1

In the beginning, y0, the husband invests D dollars in Stock No. 1. At the end of the first year, y1, he has a profit of p+q dollars.

He sells Stock No. 1 and pays a tax of q dollars on the year's profit. This leaves him D+p dollars—his original investment plus his after-tax profit.

He immediately reinvests D+p dollars in Stock No. 2, which appreciates at exactly the same rate as Stock No. 1. At the end of the second year, y2, Stock No. 2 shows a profit of r+s+t+u dollars. The profit r+s was earned on D, his original investment; the profit t+u was earned on p, his after-tax profit on Stock No. 1.

He sells Stock No. 2 at the end of the second year and pays his tax, which amounts to s dollars on his profit r+s, and u dollars on his profit t+u. After paying the tax, the husband has D+p+r+t dollars.

As the husband counts his money, we turn our attention to the wife.

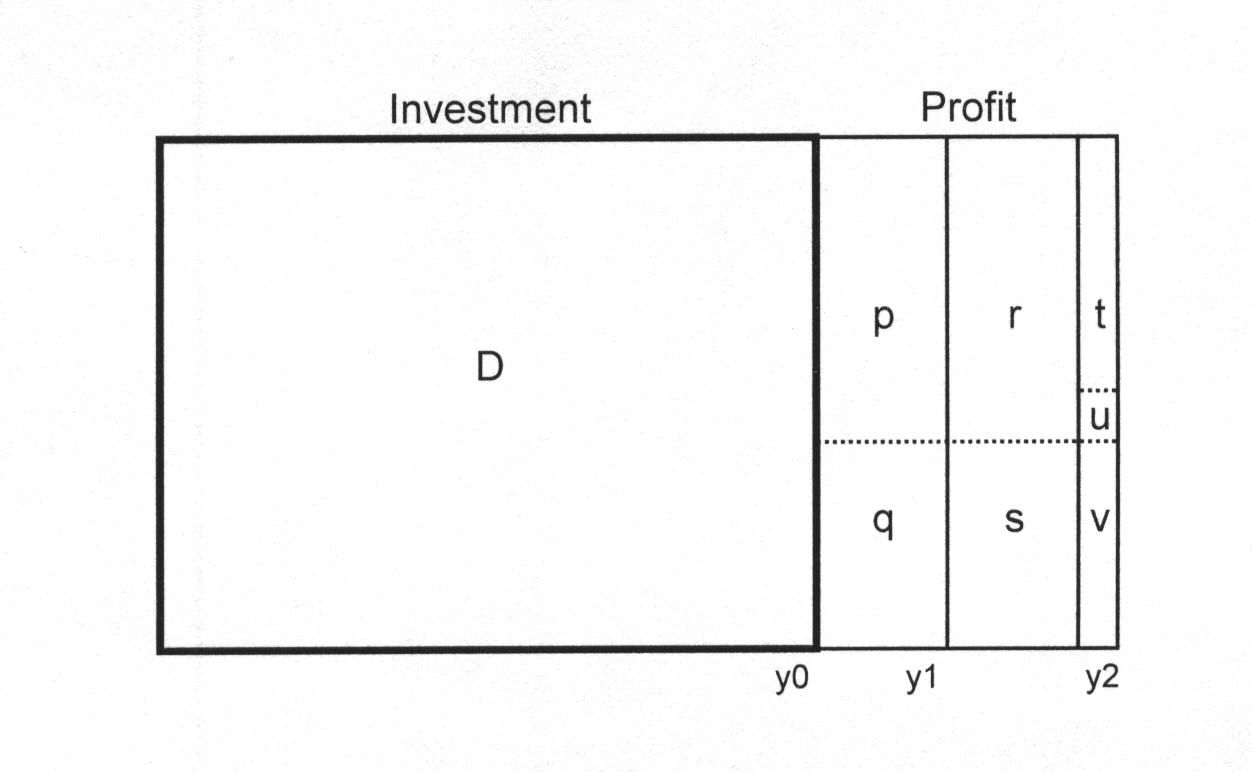

Fig. 2

In the beginning, y0, the wife—like her husband—invests D dollars in Stock No. 1. And at the end of the first year, y1, she also has a profit of p+q dollars. But unlike her husband, she does not sell; she leaves her money invested in Stock No. 1. As a result she pays no taxes at the end of year one.

By the end of the second year, y2, she has an additional profit of r+s+t+u+v. The profit r+s was earned on D, her original investment; the profit t+u+v was earned on p+q, her first-year pre-tax profit.

At this point, she does sell. She pays a tax of q dollars on p+q, her first year profit, and she pays a tax of s+v on r+s+t+u+v, her second year profit. After paying the tax q+s+v, she has D+p+r+t+u dollars.

The husband stacks his D+p+r+t dollars next to his wife's D+p+r+t+u dollars and is dismayed to see that she has u more dollars than he has.

"How is this possible?" he exclaims. "Our investments grew at the same rate, and our profits were taxed at the same rate."

"Simple," explains the wife. "By not paying the government q dollars in taxes at the end of year one, I was able to earn an after-tax profit in year two on the growth of q. My after-tax profit on that growth was u."

"I don't get it," says the husband.

"Okay, try it this way." The wife starts over.

"In year one you had a profit of p+q on Stock No. 1, but you sold it; so you had to pay q in taxes. I, too, had a profit of p+q, but I didn't sell; so I still had the government's as-yet-uncollected tax money, q, working for me.

"In year two you earned a profit on p, but I earned a profit on p+q. Your profit on p was t+u, whereas my profit on p+q was t+u+v. Your tax on t+u was u; that left you with t.

"My tax on t+u+v was v, and that left me with t+u. My t+u exceeds your t by u."

"Bummer," laments the husband.

Inside the husband's head, wheels begin to turn. "Even though my wife and I invested the same amount of money," he thinks, "and even though our investments grew at the same rate, I started the second year with less money than my wife—all because of the taxes on my first sale."

The wheels pick up speed. "To stay even with my wife," he reasons, "I'll need a higher growth rate on my investment. But how much higher?"

At that very moment, the author of this essay, who has a direct pipeline to the husband's thoughts, takes aim at the couple's doorbell and delivers a long volley of rapid rings. With no little annoyance, the husband goes to the door, opens it slightly, and peers through the crack. The author forces his right Rockport into the narrow slit, gives a hardy shove, and barges in—uninvited.

The husband and wife are aghast. But before they can so much as exhale, the intruder launches a salvo of financial verbiage that reverberates through the house.

"How much higher is a relative matter," he shouts, pulling a spreadsheet out of his pocket. "It depends on the tax rate, the trading frequency, the annualized yield on your wife's long-term investment, and the elapsed time when she closes it out. Consider Table 1!" He waves Table 1 in the air, but doesn't let them see it.

The wife, always a clever one, feigns interest and moves toward him, grabbing a poker as she passes the fireplace.

"Don't club him till I hear what he has to say," mutters the husband, annoyance suddenly taking a backseat to greed.

"There are a few assumptions behind Table 1," confesses the author, who glimpses the approaching poker and quickly adopts a deferential manner, "but they're reasonable."

"Like what?" asks the husband pointedly.

"Well, the tax rate for one thing. The table assumes a combined federal and state income tax rate of 28%—a 20% federal capital gains rate plus an 8% state income tax rate. You can't argue with that assumption."

"No, I can't," admits the husband, calming down a bit.

"That's exactly what our tax is," the wife chimes in as she adjusts her grip on the poker. "But I try to avoid tax."

"What else?" asks the husband in a nearly normal tone.

"Your trading frequency," replies the author. "The table assumes that you hold each investment for exactly one year (just long enough to qualify for the lower, long term capital gains rate) and that you immediately roll your after-tax proceeds over into another stock—which is what you've been doing."

The wife nods in agreement and relaxes her grip.

"Using those assumptions, the table shows how much higher your annualized rate of return must be for you to earn the same after-tax profit as your 'buy-and-hold' spouse."

"But we don't really know the annualized rate at which her investment will grow," complains the husband, his agitation on the rise again. "And we don't know how long she will hold it."

"True enough," agrees the author. "But this is a table. It shows a range of growth rates and holding periods. You wife's situation is likely to fall within this range, and . . ."

"All right!" The husband cuts him off. "Just show us the *#@! table."

The author hands it over.

TABLE 1.

Equivalent After-tax Rates of Return

Annualized

rate of return

for wife (buy-and-hold) 10% 11%

12% 13% 14% 15%

Tax-equivalent

annualized rate of return

for husband (trade-every-year),

assuming wife liquidates her position in:

5 years 10.5% 11.6% 12.7% 13.8% 14.9% 15.8%

10 years 11.0 12.2 13.4 14.6 15.9 17.1

15 years 11.5 12.7 14.0 15.3 16.6 17.9

20 years 11.8 13.1 14.4 15.8 17.1 18.4

"Do you mean to tell me," the husband asks after looking at the table, "that an 11% annualized return on a stock held for a decade produces more after-tax profit than a 12% annualized return on a succession of stocks traded yearly over the same period?"

"That's right," answers the author. "And if a person holds that 11% stock for two decades, it will be even harder for a yearly trader to come out ahead. He'll need a return in excess of 13%."

"And look at this!" The wife points to the last column and addresses her husband. "If I luck out and snare a stock that appreciates 15% a year, you'll never catch me."

"Well, it would be very difficult," comments the author tactfully to the husband. "If she can achieve 15%, an annual trader will have to do 2.1 points better per year over ten years—and 3.4 points better per year over twenty years—just to tie her."

"Do you think you can do that consistently?" the wife asks her mate, giving him a playful nudge with her elbow.

"Probably not," her husband acknowledges. "Not if these figures are correct. But how do I know they are?"

"If your wife will put down her poker, I'll prove it. But for your own safety, you'd better take a seat. When I gave this explanation to an investment club, people were dropping like hailstones."

"Say, you buy a stock," the author says to the wife as she and her husband settle in. "And, say, its price appreciates a% annually."

"Oh, no!" whispers the husband. "We're going to hear a bunch of mathematical abstractions."

"Just listen," counters the wife. "It may improve your return.

"In one year, your investment will be worth 100% of its original value plus another a%. Since 100% equals 1, your investment's future value factor for one year is 1+a%. In other words, if you multiply the number of dollars you originally invested by the factor 1+a%, you'll get the value of your investment one year into the future."

"Basic finance," says the wife.

"Suppose you hold your investment for y years. The future value factor for y years is (1+a%)y. At the end of y years, your investment will be worth (1+a%)y times its original value."

"That's y different (1+a%), all multiplied together," mimes the wife, who has a knack for winning at charades: "If y happens to be 3 years, it's (1+a%) * (1+a%) * (1+a%)."

The husband shifts in his LA-Z-Boy. "Let's hear about profit."

"At the end of y years, your profit will equal your original investment times the factor [(1+a%)y -1]. That - 1 at the end is there to subtract out the money you originally invested.

"And when you sell your stock, the profit will be taxed at a rate of t%."

"I try to avoid tax," reaffirms the wife.

"The percent of the profit remaining after taxes will be 1-t%. In dollars, the after-tax profit will be your original investment times the factor [(1+a%)y -1](1-t%)."

"Are you saying that this ugly mathematical expression describes the net profit of my lovely wife?" inquires the husband, leaning forward.

"Yes, I am."

"And is there an expression that describes my net profit?"

"It's even uglier."

"Naturally," says the wife.

The author presses on. "Let's assume that there is a second investor, an active trader. This guy buys a stock, and its price appreciates b% over a year. After one year, he sells it, pays his taxes, and reinvests his residual funds in another stock. Say, he does this year after year."

"Like I do," says the husband.

"And, say, each investment earns him the same annual return, b%. His after-tax profit at the end of the first year is his initial investment times the factor b%(1-t%). The after-tax money available for reinvestment at the start of the second year is his initial investment times the factor [1+ b%(1-t%)].

"Now let's jump into the future."

"How far?" asks the husband, suppressing a yawn.

"How about y years?" suggests the wife.

"Fine," says the author. "At the end of y years, the total after-tax profit on his original investment is the investment times the factor { [1+ b%(1-t%)] y –1}.

The husband barely catches himself as his eyelids drop and his chin plummets to his chest.

"We almost there," responds the author. "And I think you'll like the conclusion. It's the answer you were after when I rang the doorbell."

" 'When you pummeled . . .', " corrects the wife, eyeing the poker again.

The author, on his last lap to a spectacular finish, ignores her. "Let's recap. Two investors start with the same amount of money. Both stay invested for y years. What annualized rate of return, b%, does the active trader need in order to earn the same after-tax profit as the long-term investor?

"To find out, we'll set the trader's after-tax profit factor { [1+ b%(1-t%)] y –1} equal to the long-term investor's after-tax profit factor [(1+a%)y -1](1-t%), and we'll solve for b%.

"The answer is"—a passing car honks:

b% = ( { [(1+a%)y -1](1-t%) +1}1/y –1) / (1-t%)

The husband and wife sit there. Motionless.

The author bows politely. He mops his brow. Then he turns and in measured stride heads for the door.

"What's that little 1/y superscript?" the husband calls out.

"That's the yth root of the stuff inside {}," the author answers back over his shoulder.

"y is the number of years," mimes the wife.

The door thumps shut. The engine of an '86 Toyota springs to life.

"But how do I figure {}1/y?" shouts the husband through an open window.

The author's voice, accompanied by the faint putt of a Midas muffler, trails off in the distance. "Buy a pocket calculator."

"They're really quite cheap," mimes the wife.

Postpone tax and earn a compounding net profit on the government's as-yet-uncollected money.

© 2000 ThinkingApplied.com

![]()